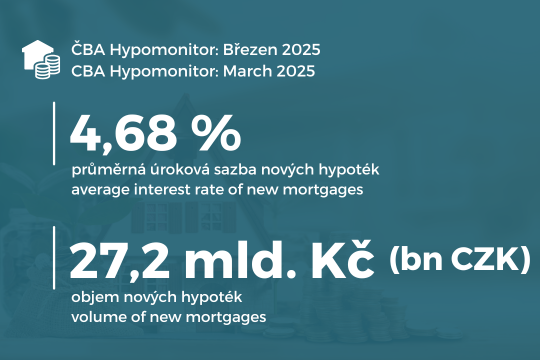

CBA Hypomonitor: Spring mortgage boom with a slight drop in interest rates

March continued the strong growth in new mortgage originations

Table 1: Summary of mortgage origination volumes and average interest rates for March 2025

|

|

Volume |

Number of |

Rate |

|

|

|||

|

Total |

32,8 |

8 382 |

4,68 |

|

New loans |

27,2 |

6 680 |

4,68 |

|

of which: |

|

|

|

|

for purchase |

21,3 |

5 187 |

4,67 |

|

for construction |

4,4 |

1 114 |

4,66 |

|

Other |

1,4 |

379 |

4,91 |

|

Refinanced from another institution |

4,4 |

1 365 |

4,65 |

|

Refinanced internally |

1,2 |

337 |

4,67 |

|

Source. |

|

|

|

"In particular, we see increased dynamics in the growth of sales, which was also contributed by the February special offer of some banks, when most of the contracts from this offer were signed in March.Current figures from the mortgage and real estate market also show that despite a relatively slight decline in interest rates, people's demand for their own housing is growing significantly," says Ondřej Šuchman, mortgage manager at Komerční banka.

The average mortgage rate continues its downward trend

Chart 1: Average mortgage rate - new business

"The economic recovery and falling interest rates are supporting demand for mortgage loans and the mortgage market is thus thriving. The big unknown for the future, however, is the uncertainty coming into the economy due to the completely unreadable US tariff policy, which has the potential to affect interest rates in both directions," says Petr Gapko, Chief Economist at MONETA Money Bank.

"The US tariffs are interpreted by the markets as a disinflationary factor across the US, Europe and therefore also in the case of the Czech economy. It remains to be seen how quickly and whether market expectations will translate into a decision by the Czech National Bank, which is likely to remain vigilant in the near term due to continued inflationary pressures from the services sector.If so, this could pave the way for mortgage rates to fall to 4.25% during the second half of this year," adds Jaromír Šindel, chief economist at the Czech Banking Association.

Average mortgage size rose further in January due to construction loans

Impact on the average instalment

Chart 2: Average amount of new mortgages actually granted by purpose

Table 2: Illustration of the average monthly mortgage payment by length of repayment and interest rate

|

Average size of a new mortgage in CZK: |

|

|

4 065 955 |

||||

|

Average interest rate in %: |

|

2,0 |

3,0 |

4,0 |

4,68 |

5,0 |

6,0 |

|

|

|

|

|

Monthly instalment: |

|||

|

Mortgage maturity in years: |

15 |

26 160 |

28 080 |

30 080 |

31 490 |

32 150 |

34 310 |

|

20 |

20 570 |

22 550 |

24 640 |

26 130 |

26 830 |

29 130 |

|

|

25 |

17 230 |

19 280 |

21 460 |

23 030 |

23 770 |

26 200 |

|

|

|

26,5 |

16 470 |

18 540 |

20 750 |

22 330 |

23 090 |

25 560 |

|

|

30 |

15 030 |

17 140 |

19 410 |

21 050 |

21 830 |

24 380 |

|

Source: CBA [1] |

|||||||

|

Note: the coloured column corresponds to the interest rate of the latest CBA Hypomonitor, other rates are illustrative; the coloured row corresponds to the average maturity of new mortgages according to CNB data; amounts are rounded to tens of crowns. |

|||||||

Chart 3: Illustrative comparison of the average monthly mortgage payment with a year ago, depending on the interest rate, mortgage size and maturity in years

Statistical annex

Mortgage market in 2024: record growth of 83%

Chart 2: Annual volume, number and average amount of mortgages granted between 2020 and 2024

CBA publishes summary statistics for the entire banking market

- Purchase of real estate

- Property construction - including property renovation

- Other new arrangements - only new loans that are in no way related to the purchase or construction of the property, e.g. so-called American mortgages, settlement of a JVM, repayment of the purchase price, settlement of an inheritance share, settlement of a cooperative share, etc.

- an increase in the agreed amount

- changes such that the original loan has been refinanced/converted into a new loan within the reporting entity. This is a genuinely new contract and not, for example, just a new arrangement in the context of a refixation of an existing contract. Therefore, the volume of such loans in the CBA statistics is lower than 'other new arrangements' in the Czech National Bank statistics.