The Czech economy accelerated its quarter-over-quarter growth to 0.4% in the second quarter, up from 0.2% previously. The result was in line with the pace of growth across the entire eurozone but once again fell short of the CNB’s forecast, which may temper its hawkish stance. GDP growth in the second quarter was driven by household consumption and foreign trade, while investment activity held the economy back. The Czech Banking Association’s (CBA) forecast for the second half of the year anticipates only a slight further acceleration.

The brisk pace of lending activity continues, and payment behavior is very good

Jaromír Šindel

03. 08. 2026

The CNB is likely to keep the two-week repo rate at 3.75% in August. However, the ECB’s wait-and-see approach is not a definitive guide for Czech monetary policy: domestic core inflation, the labor market, and lending activity are having a more inflationary effect. However, it is not just mortgages that are driving Czech lending; there is also a noticeable recovery in investment loans, which could ease inflationary pressures on the supply side. If service prices start rising again in July and August, the Bank Board may raise the rate to 4% on September 17. Markets are pricing in interest rate hikes by both the CNB and the ECB this fall.

Jaromír Šindel

24. 07. 2026

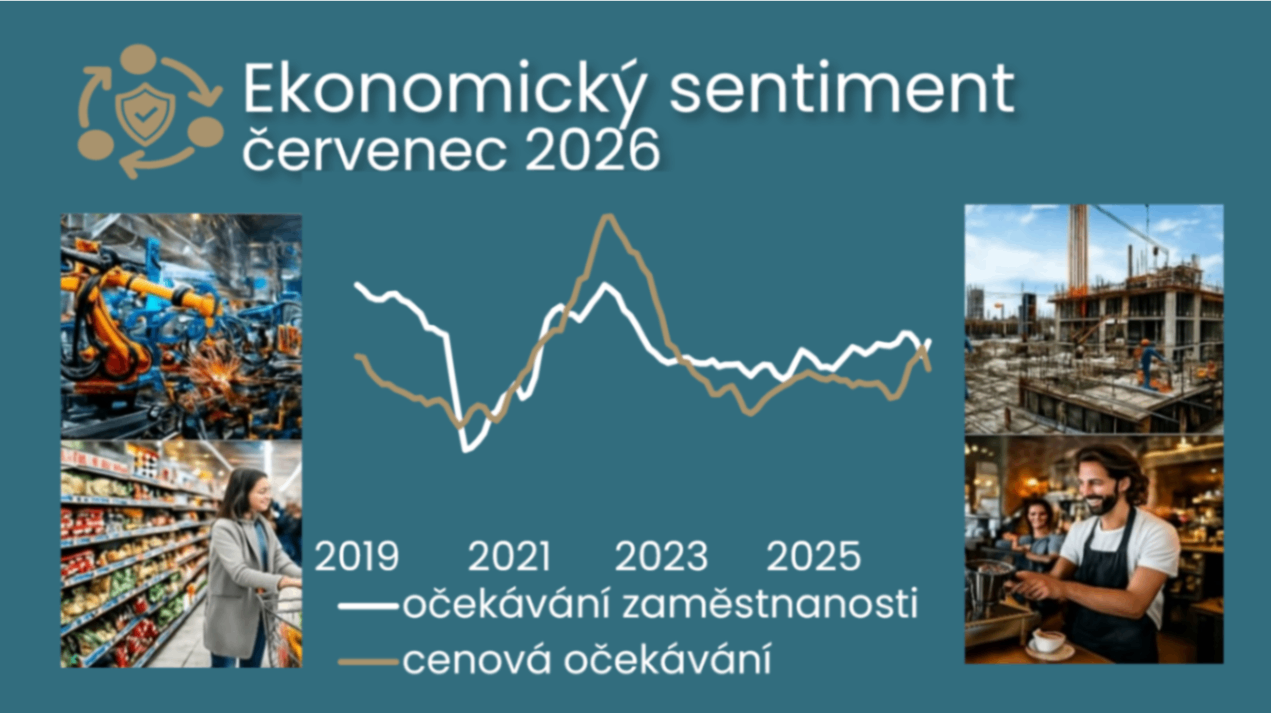

Although confidence in the Czech economy improved only slightly in July, it did so for the second month in a row, confirming its resilience despite heightened geopolitical uncertainty. Positive signals are coming mainly from the industrial sector, where assessments of demand and capacity utilization are improving, as well as from employment expectations. At the same time, declining price expectations are easing the CNB’s concerns about persistent inflationary pressures; however, the return of higher oil prices does not yet give the central bank a reason to deviate from its rather hawkish communication.

Jaromír Šindel

23. 07. 2026

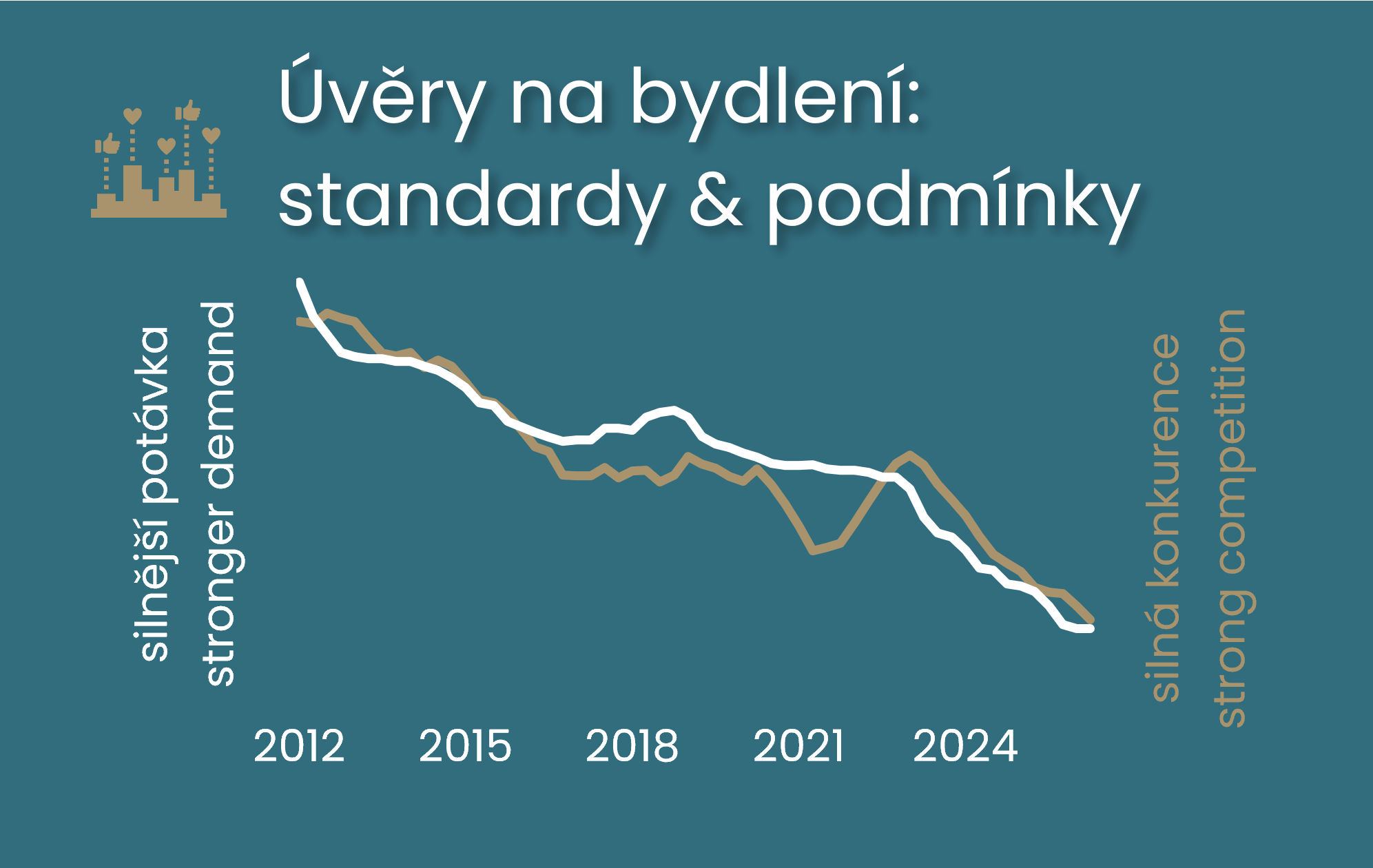

The CNB’s survey of banks’ lending conditions for the second quarter came as no surprise; the most significant change concerned housing loans. The central bank’s stricter criteria for investment mortgages tightened not only the banks’ lending requirements. In line with historical experience, this supported demand, likely temporarily. The impact on lending conditions was partially offset by lower bank margins and more favorable repayment terms. In an environment of continued strong competition, the stronger demand helped mitigate the impact of the spike in market interest rates on mortgage rates, which consequently rose more modestly. However, expectations of weaker demand for housing loans in the third quarter are changing this narrative. Surveys on consumer and business loans are also likely to keep the CNB’s outlook on the hawkish side.

Jaromír Šindel

17. 07. 2026

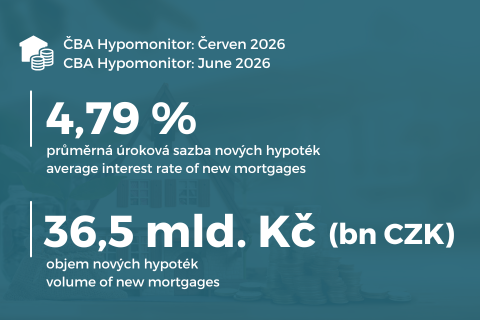

The average interest rate on new mortgages rose to 4.79%, while the average mortgage amount fell back below 4.7 million crowns. Banks and building societies issued new mortgages (excluding refinancing) totaling 36.5 billion crowns. After months of exceptionally strong mortgage activity, June saw a clear return to the robust normal levels seen in the second half of last year. In the first half of the year, the volume of new mortgages reached 216 billion crowns, which is 66 billion more than last year. Higher market interest rates and expensive real estate remain the main obstacles.

Miroslav Zámečník

02. 07. 2026

Commentary by Miroslav Zámečník, Chief Advisor to the Czech Banking Association

Jaromír Šindel

30. 06. 2026

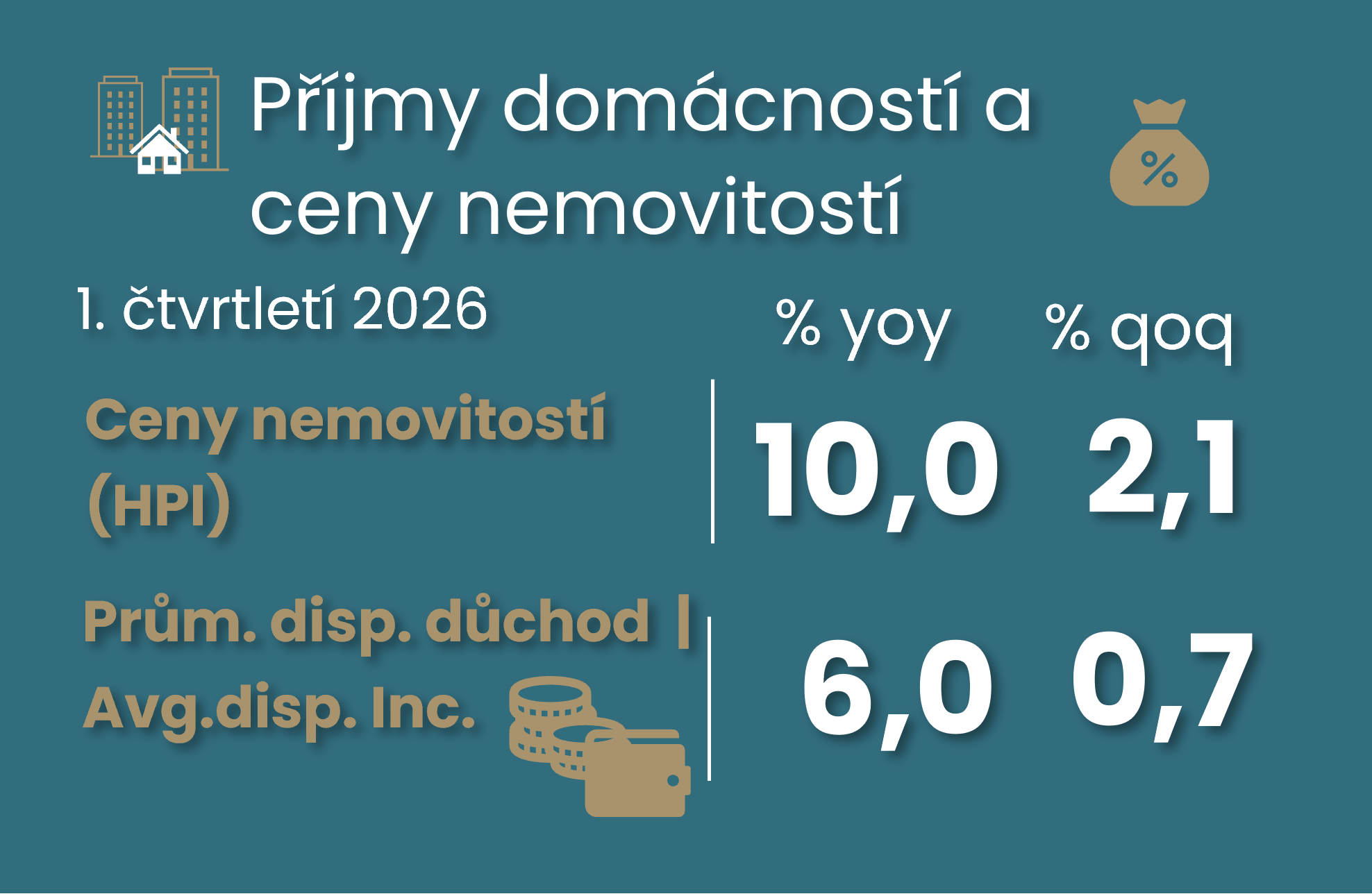

The Czech household savings rate remained at 20% in the first quarter of this year, still high even by international standards. Household disposable income slowed to 0.7% quarter on quarter, while property prices continued to rise by roughly 2%. The GDP revision showed weaker household consumption, but also a less negative productivity story thanks to stronger value added in industry. However, despite somewhat more moderate growth in the past, unit labour costs remain on a strong upward trend, which, together with high core inflation growth, is unlikely to bring a dovish turn at the CNB. That said, my interpretation of the new data from the Czech Statistical Office, especially for the first quarter, is significantly affected by the alignment of quarterly figures with the new annual data for 2025. The next quarterly release may therefore bring yet another story about the economy in the first quarter.

Jaromír Šindel

24. 06. 2026

Economic confidence improved slightly in June. Stronger sentiment among households and manufacturers outweighed continued weakness in retail trade, although retail conditions may improve over the coming months. At the same time, the services sector points to higher risks for both unemployment and core inflation—that is, inflation excluding the volatile prices of energy and food. For the Czech National Bank (CNB), the June sentiment survey suggests a need for caution, reflecting stronger household demand and a renewed rise in price expectations in services.

Jaromír Šindel

18. 06. 2026

The Bank Board raised the interest rate by a quarter of a percentage point to 3.75%. Unsurprisingly, the main reason was the continued high growth in demand-driven, or “core,” inflation, which reflects stronger wage growth. However, the decision also reflects stronger credit growth and rising real estate prices. I view today’s decision as an effort by the central bank to keep consumer inflation in line with its inflation target over the longer term, which is not possible with core inflation hovering around 3%. Today’s decision reduces the risk premium—or rather, the uncertainty regarding the credibility of achieving the inflation target and the central bank’s independence. Below, I discuss further possible steps and their implications for the economy and the banking sector. If energy prices remain lower, this will reduce the likelihood of the CNB reaching a 4% interest rate. However, core inflation must lose momentum for the CNB to avoid reaching that level.

Jaromír Šindel

15. 06. 2026

While the growth in actual apartment prices slowed to approximately 2.5% quarter-over-quarter in the first quarter, with significantly different trends between Prague and the rest of the country, However, even the current milder growth does not yet suggest a significant slowdown in year-over-year apartment price growth this year. Asking prices do not indicate this yet. This is especially true if there is a shift of pent-up demand for more expensive Prague apartments to the regions. Data from Flat Zone show an average transaction price of CZK 98,000 per square meter for apartments in the first quarter. Stricter criteria for so-called investment mortgages, as well as higher mortgage interest rates, may further cool the real estate market; however, higher wage growth keeps real mortgage interest rates negative.

Jaromír Šindel

12. 06. 2026

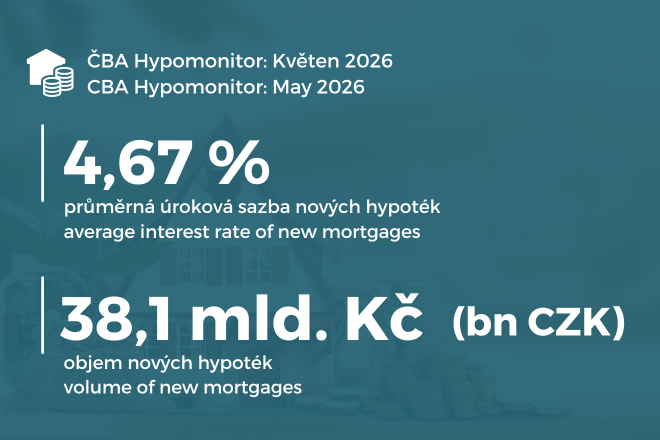

In May 2026, banks and building societies actually issued new mortgages (excluding refinancing) totaling CZK 38.1 billion.

Jaromír Šindel

10. 06. 2026

Consumer price inflation slowed to 2.1% year on year in May, close to the CNB's target. However, domestic inflationary pressures continue to operate beneath the surface. Core inflation remained at 2.9% y/y and its short-term dynamics suggest an acceleration closer to 4%. The latest economic numbers do not suggest a reversal and thus a relief of the inflationary nature of the Czech economy due to strong wage growth and weak productivity growth. This constellation, together with the ongoing Iranian conflict, reinforces the rationale for a 0.25 percentage point increase in the central bank's interest rate to 3.75% at the June meeting. This will not be an easy decision for the Board.

Jaromír Šindel

08. 06. 2026

April's monthly figures open the way for stronger GDP growth in Q2 for now, after slowing to 0.2% q-o-q in Q1. The April industrial numbers are 1.8% above the first quarter average thanks to the April rebound. Despite a slight April decline, the construction sector is on an uptrend, thanks in part to strong housing starts, which rebounded from weaker building permits. Moreover, its sentiment does not suggest a change in trend. Foreign trade reached its lowest surplus below CZK4bn since the end of the energy crisis in 2022. However, this mainly reflects higher non-energy imports, while export activity also showed solid growth thanks to ICT. Thus, net exports are unlikely to drive GDP, similar to the first quarter when their weaker contribution was offset by stronger investment activity.

Jaromír Šindel

04. 06. 2026

The countercyclical capital buffer should rise to 1.5% from July 2027, which will increase banks' total capital requirements to around 17% next year, in response to continued growth in lending to households and firms and lower perceived risks in the banking sector. Again, we are also seeing stronger wage growth outpacing productivity. In the case of rising investment credit, however, this is a dilemma for macroprudential policy. In addition to the financial cycle, the results of stress tests, including concerns about the interconnectedness of the banking and government sectors, are likely to have factored into the decision. It leaves mortgage rules unchanged.

Jaromír Šindel

04. 06. 2026

April's decline in retail sales was largely the result of a correction of the previous strong growth in fuel and food. Although the correction after a strong March was also evident in core retail sales, they maintained their growth momentum, confirming the continued willingness of households to spend, supported by real wage growth and credit activity. However, factors are beginning to emerge in the second quarter that may slow the pace of household consumption. We discuss three of them below - real wage growth, credit activity and retail bonds.

Jaromír Šindel

04. 06. 2026

Consumer price inflation slowed to 2.1% in May, surprising at a more moderate pace than the market had expected. However, some of the factors now dampening inflation may not be permanent. This is particularly true for food prices, which may be affected by rising global commodity prices in the months ahead. At the same time, strong wage growth of 8.1% year-on-year is divorced from labour productivity, creating pressures for higher core inflation. It is the contradiction between low headline inflation and persistent domestic inflationary pressures that poses a non-trivial economic and political dilemma for the CNB.

The CBA Forecast is compiled quarterly as a consensus of forecasts from selected domestic banks. A basic summary of the current CBA Forecast, presented in a few figures and comments, is outlined below; detailed information can be found in the “CBA Forecast” section.

Macroeconomic Forecast for the Second Quarter of 2026

CBA Macroeconomic Forecast 2Q26 (Part 2): interview with Helena Horská

25. 05. 2026

The domestic economy will grow by 2% this year. The CBA forecasting panel worsened the outlook due to the events in Hormuz. The forecast from the first quarter predicted growth of 2.6%. Consumer inflation should accelerate towards the upper limit of the inflation target at the end of this year.

CBA Macroeconomic Forecast 2Q26 (Part 1): interview with economist Petr Gapek

21. 05. 2026

According to the CBA's forecasting panel, Czech economic growth will slow to 2% this year. The worsening outlook is mainly related to the war in the Middle East and the closure of the Strait of Hormuz. Consumer inflation is expected to accelerate towards the upper boundary of the inflation target at the end of this year, with average growth of 2.5% this year.

MACROECONOMIC FORECAST OF THE CZECH REPUBLIC 2Q 26

20. 05. 2026

May 2026: Economic growth slowing to 2% with risks on many fronts, 2.4% growth next year

Chief Economist of the Czech Banking Association (CBA)

Chief Economist of the Czech Banking Association (Part 15)

Jaromír Šindel

31. 07. 2026

This time, the discussion focused on current developments in the Czech economy, the situation in industry, household consumption, and the high savings rate. CBA Chief Economist Jaromír Šindel also discussed June’s very low inflation, the Czech National Bank’s monetary policy, and the expected trajectory of interest rates in light of domestic and foreign economic risks.

Chief Economist of the Czech Banking Association (Part 14)

Jaromír Šindel

11. 06. 2026

This time, we discussed the performance of the Czech economy and the slower quarter-over-quarter GDP growth, which was primarily caused by a negative contribution from foreign trade. Jaromír Šindel, chief economist at the Czech Banking Association (CBA), also spoke about stagnating productivity and the related inflation trends. We also discussed possible steps the central bank might take.

Jaromír ŠindelChief Economist CBA

Jaromír Šindel is the Chief Economist of the Czech Banking Association, where he uses his extensive experience in the field of macroeconomic analysis and forecasting. Prior to that, he worked for more than 17 years as the Chief Economist at Citibank. In 1999 - 2004, he received a master’s degree from the University of Economics Prague with a major in economic policy and continued to focus on this field during his doctoral studies, which he completed in 2011.

During his time at Citibank (2007-2024), he worked mainly on macroeconomic analysis with a focus on economic trends in the Czech Republic, Slovakia and Slovenia. He prepared forecasts of economic developments and economic policy, including the impact on financial markets. Related to this, he also monitored global economic and political trends and their impact on the local economic situation.