CBA Hypomonitor: Banks granted the most mortgages in June this year

Average interest rate fell to 5.06%

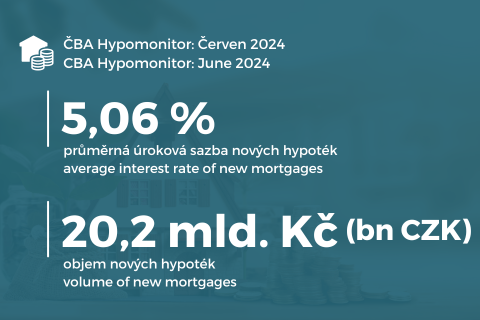

Prague, July 12, 2024 - Banks and building societies granted mortgage loans worth CZK 24.2 billion in June this year, of which actual new loans amounted to CZK 20.2 billion, slightly exceeding the May level. The June volume of new mortgages granted is thus the highest this year and, together with May, is above CZK 20 billion for the first time in more than two years. In month-on-month terms, the volume of mortgages granted rose by only a slight 0.6%, while in year-on-year terms the growth slowed from over 90% in May to around 70%, which is also due to the higher comparison base from last year. The figures from the mortgage market this year thus confirm its recovery, with mortgage volumes already above 2020 levels in the last two months. The average mortgage rate for new loans continued to fall, but only cosmetically, from 5.07% to 5.06%. The average mortgage size further increased to 3.74m. CZK. The above information is derived from data from the CBA Hypomonitor, which captures data from all domestic banks and building societies providing mortgage loans.

The volume of mortgages granted in June slightly exceeded May's value

Banks and building societies granted mortgages to households in June in the volume of 24.2 billion CZK, according to CBA Hypomonitor. CZK 24bn. Thus, the volume of mortgages granted increased by CZK 0.5 billion, i.e. 2.2%, month-on-month and was at its highest level since March 2022. Despite the month-on-month slowdown, the June volume of mortgages granted remains favourable and confirms that the recovery in mortgage activity continues this year. Year-on-year growth has slowed from 92% to 73%, driven by an already higher comparative base last year as well as an exceptionally strong previous month. In the first half of the year, banks granted mortgages worth CZK 117 billion, an 80% year-on-year increase. However, compared to the first half of 2020, the volume is still roughly a tenth lower.

"Demand for mortgages has been growing in recent months, partly because of fears that house prices will start to rise again. Although activity may slow slightly during the coming summer months due to the holiday season, this does not change the fact that the outlook for this year remains positive in terms of mortgage originations," says Marek Richter, head of mortgage services at Air Bank.

Table 1: Summary of mortgage origination volume and average interest rates for June 2024

|

|

volume (billion CZK) |

Number |

|

|

|

|||

|

Total |

24.2 |

6,697 |

5.06 |

|

New

credits |

20.2 |

5,403 |

5.06 |

|

from

of which: |

|

|

|

|

on

purchase |

16.2 |

4,234 |

5.05 |

|

on

construction |

3.1 |

861 |

5.07 |

|

other |

1.0 |

308 |

5.23 |

|

Refunded

from another institution |

3.3 |

1 047 |

5.04 |

|

Refunded

Internally |

0.7 |

247 |

5.12 |

|

|

|

|

|

The volume of actual new mortgages granted without refinancing reached CZK 20.2 billion in June. Month-on-month, the volume increased by 0.6%, i.e. it was mostly flat. The volume of refinanced loans (internally or from another institution) amounted to CZK 4 billion after CZK 3.6 billion in May. The share of refinanced loans in total mortgage originations was 16.5% in June, slightly above the annual average of 15.9%.The number of new mortgages originated reached 5,403, slightly below May's level, the second highest level this year and, together with May, the highest level since March 2022, when just under 7,500 mortgages were originated.

"The latest figures from the mortgage market confirm its gradual recovery and the volume of new mortgages in recent months is among the highest in the last two years. The first half of the year has already seen a similar volume of mortgage originations to the first half of 2020, but the number of mortgages itself was still a quarter lower," says Jakub Seidler, chief economist at the Czech Banking Association.

The average mortgage rate fell slightly further and remains the lowest since June 2022

The interest rate on actual new mortgage loans fell cosmetically from May's 5.07% to 5.06%, further reducing the rate of month-on-month decline from previous months. This development is attributable to volatile market interest rates, which started to rise again in mid-March and, despite their volatility, were at the highest levels of the year. Realised interest rates, as opposed to bid prices, reflect the actual real interest rate on signed mortgage contracts.

"The gradual reduction of rates by the central bank has had the greatest impact on the decline in interest rates on mortgages with short fixations. This allows clients to currently take advantage of 1-3 year fixings and to respond flexibly to the new conditions in the medium term. The decline in rates on longer fixings will not be as rapid this year, also due to the ongoing uncertainty about the further development of inflation," states Michael Pupala, CEO of Blue Pyramid Building Savings Bank

Graph 1: Average Mortgage Rate - New Business

Mortgage rates react with a lag of several months mainly to the evolution of market interest rates for longer maturities. They are influenced by a number of factors - not only the expected development of CNB base rates, but also the outlook for inflation, economic developments and the dynamics of similar interest rates abroad. The aforementioned market interest rates for longer maturities [1] started to fall since last October due to growing market expectations of rate cuts by the major central banks, but these expectations turned around again in March this year, when market rates started to rise again after several months. This development has partially closed the existing scope for mortgage rates to fall more quickly, although markets are currently volatile and there have been alternating periods of falling and rising mortgage rates in recent months. The release of lower-than-expected June inflation led to an intensification of market bets for a faster fall in interest rates, to which longer-term rates responded, falling to their lowest level since late March.Compared with last month, they are roughly 0.5 percentage point lower, and their average June value was about a tenth below the average for this year.

Average mortgage size hit a new record high

The average mortgage size continued to rise in May, rising from 3.63m to 3.74m. CZK. Since April, the average mortgage amount has thus exceeded the previous record level set in November 2021 of CZK 3.46m. The gradual decline in mortgage rates or the relaxation of macroprudential income limits by the CNB, together with a gradual increase in real household incomes, is making it possible to achieve a higher mortgage. The mortgage rate is also related to the evolution of house prices, which were 10% higher in Q1 this year than in the last quarter of 2021.

Table 2 shows the scenarios of the evolution of the monthly payment for different mortgage maturities. It shows that an increase in mortgage rates by one percentage point means an increase in the monthly payment of approximately CZK 1,500 to CZK 2,000 for an average mortgage size. Compared to the 2% interest rate that was common on the market in earlier years, the current mortgage rate means an increase in the monthly payment for an average mortgage of approximately CZK 6,000. [2] The mortgage payment of one million crowns with a 30-year maturity at current interest rates is around CZK 5.5 thousand.

[1] These are mainly long-term interest rate swaps (IRS), which reflect the price of money in longer maturities, for example 2 to 10 years.

[2] The table is available in the xls file attached on the CBA Hypomonitor website

Table 2: Average monthly mortgage payment by length of term and interest rate

|

Average new mortgage size in CZK: |

|

|

|

||||

|

Average interest rate in %: |

|

2.0 |

3.0 |

4.0 |

5.06 |

6.0 |

7.0 |

|

|

|

|

|

Monthly installment: |

|||

|

Mortgage term in years: |

15 |

24,068 |

25,828 |

27,665 |

29,692 |

31,561 |

33,617 |

|

20 |

18,920 |

20,742 |

22,664 |

24,806 |

26,795 |

28,997 |

|

|

25 |

15,852 |

17,736 |

19,741 |

21,994 |

24 097 |

26,434 |

|

|

|

30 |

13,824 |

15,768 |

17,856 |

20 214 |

22,424 |

24,883 |

|

|

|||||||

|

Note: the color bar corresponds to the interest rate of the last CBA

Hypomonitor, other rates are illustrative |

|||||||

For the full year 2023, activity in the mortgage market fell by a quarter

For the full year 2023, banks and building societies granted mortgage loans in the volume of CZK 150 billion, of which net new loans without refinancing amounted to CZK 124 billion. This is mainly due to the fact that the first half of 2022 was still strong in terms of mortgage originations and the higher comparative base from this period is thus affecting the year-on-year comparison. As a result, there were 50% fewer mortgages originated year-on-year in the first half of 2023 and over 50% more in the second half of 2023. Compared to the pre-pandemic years 2017-2019, the volume of mortgages originated in 2023 was roughly one-third lower.

Figure 2: Full-year volume and number of mortgages originated from 2021 to 2023

Source: CBA Hypomonitor

CBA publishes summary statistics for the entire banking market

The Czech Banking Association publishes new summary statistics from the housing market in cooperation with its member banks. These are mainly volumes and numbers of new and refinanced mortgages and the respective interest rate. These statistics are published by the CBA in aggregate form for the entire banking sector on a regular basis around the middle of each month. All domestic banks and building societies providing mortgages in the Czech Republic participate in the survey. The data are available from January 2020 in the attached file on www.cbaonline.cz, where the relevant statistics can also be found separately for banks and building societies. The above figures are for the sector as a whole, which can also be viewed in simple graphical form on the website cbamonitor.cz.

CBA Hypomonitor Methodology

CBA Hypomonitor divides mortgage loans made by banks and building societies to households into several categories to distinguish new loans from refinanced or internal refixations. New loans are then reported in categories according to the purpose of the loan:

1. New loans

These are loans whose entire volume enters the economy for the first time. This category does not include loan consolidation or loan refinancing. They fall into three categories:

- Buying real estate

- Real Estate Development - including property renovation

- Other New Arrangements - only new loans that are in no way related to the purchase or development of real estate, e.g. so-called. American mortgages, settlement of a JJM, reimbursement of the purchase price, settlement of an inheritance share, settlement of a cooperative share, etc.

2. Refinanced loans from another financial institution

These are loans that have been originated by refinancing one or more loans from a financial institution other than the reporting one. Regardless of the amount refinanced and regardless of the amount of any increase, the total amount of the newly originated loan is reported in this category.

3. Increased or internally refinanced loans

These are loans that were already part of the reporting entity's portfolio in the previous reporting period and have experienced any of the following changes during the reporting period:

- increase in the agreed amount

- there have been changes such that the original loan has been refinanced/transferred to a new loan within the reporting entity. This is a genuinely new contract and not, for example, just a new arrangement in the context of a refixation of an existing contract. Therefore, the volume of such loans in the CBA statistics is lower compared to "other new arrangements" in the Czech National Bank statistics.

The following banks and building societies provide data for the CBA Hypomonitor: Air Bank, Banka Creditas, Česká spořitelna, ČSOB, ČSOB Stavební spořitelna, Fio banka, Hypoteční banka, Komerční banka, mBank, Modrá pyramida, MONETA Money Bank, MONETA Stavební spořitelna, Oberbank, Raiffeisen stavební spořitelna, Raiffeisenbank, Stavební spořitelna České spořitelna, UniCredit Bank.